Joint Economic Forecast Autumn 2022: Energy Crisis: Inflation, Recession, Welfare Loss

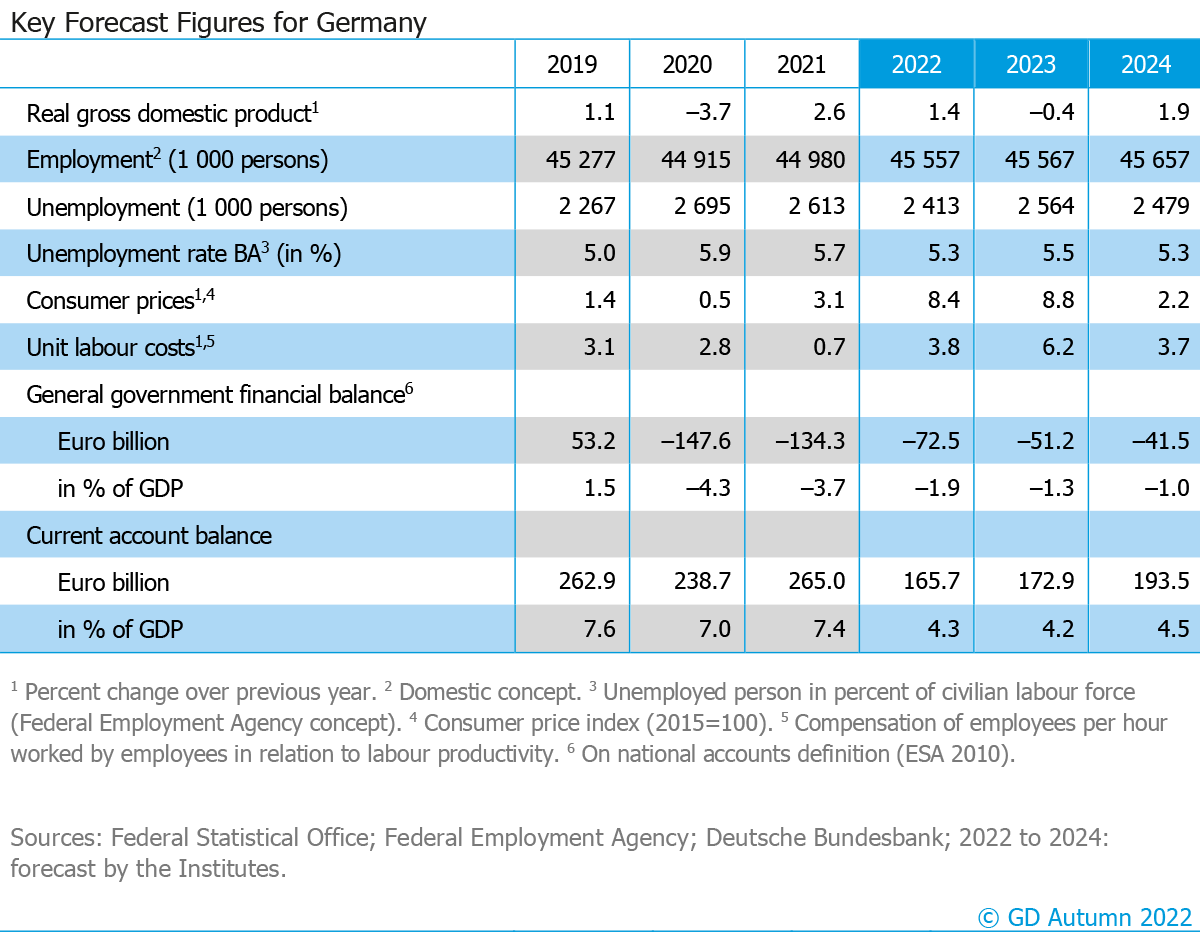

The German economy is being hit hard by the crisis on the gas markets. Skyrocketing gas prices are drastically increasing energy costs and are accompanied by a massive macroeconomic withdrawal of purchasing power. This is not only dampening the still incomplete recovery from the coronavirus crisis, but also pushing the German economy into recession. Overall, the institutes expect gross domestic product to expand by 1.4 percent this year and contract by 0.4 percent next year. In 2024, GDP will expand at an annual average rate of 1.9 percent.

The reduced gas supplies from Russia have eliminated a significant portion of the supply and also increased the risk that the remaining supply and storage volumes in winter are not sufficient to meet demand. As a result, gas prices skyrocketed in the summer months. Companies have already started to cut their gas consumption noticeably. Even though the institutes do not expect a gas shortage in normal weather conditions for the coming winter, the supply situation remains extremely tight.

Inflation Breaks Records

Increased energy prices reinforce the upward pressure on prices that had already begun in the coronavirus pandemic. As a result of the Covid-19 protection measures, international supply chains were significantly disrupted, which was accompanied by rising prices for raw materials and intermediate products. These price increases were passed on to consumers. Very expansive monetary and fiscal policy further intensified the upward pressure on prices. As a result, consumer prices are rising across the board. In the meantime, inflation rates have reached levels that exceed even the high-inflation phases in the 1970s and early 1980s. All in all, inflation this year is at an average rate of 8.4 percent, the highest since the Federal Republic of Germany was founded. In the coming year, inflation will likely rise even further to an average of 8.8 percent for the year. For 2024, the institutes expect inflation to calm down again and to be only slightly above the ECB’s target rate of 2 percent.

The sharp rise in consumer prices is eroding the purchasing power of private households. The fact that private consumption nevertheless expanded significantly in the first half of the year is due to private households saving less. In the process, some are probably also drawing on the funds accumulated during the pandemic, not least to enjoy more of the services they had to do without during this period. In the meantime, however, the outlook for consumption has clouded over considerably. Inflation, which remains high due to the delayed pass-through of gas and electricity prices, will cause real disposable incomes to fall significantly into the coming year. The massive withdrawal of purchasing power is likely to cause private consumption to decline until the summer of next year and not recover until the second half of the forecast period.

Companies are affected very differently by the sharp rise in energy prices. At present, many are managing to pass on the cost increases to customers. Energy-intensive companies, above all in the chemical industry, have been significantly more affected by the crisis on the gas market. To cut costs, many companies have started to reduce their gas consumption. On the one hand, this has been done by substituting gas with other production factors. On the other hand, production has been cut back significantly, especially in the chemical industry. As a result of declining purchasing power among private households, the consumer-related sectors of the economy are also coming under increasing pressure.

Temporarily Declining Employment

The labor market is having a stabilizing effect on economic development. Demand for new workers is likely to remain low in view of the crisis-related weak phase. However, due to the shortage of skilled workers in many areas, companies will endeavor to maintain existing staff levels, so that employment is likely to fall only slightly for the time being. As the recovery progresses, employment is then expected to increase again. The average annual unemployment rate in 2023 and 2024 will be 5.5 percent and 5.3 percent respectively, compared with 5.3 percent in the current year.

Public Budgets Remain in the Red

The general government budget deficit was 3.7 percent as a share of GDP in 2021 due to extensive pandemic-related fiscal measures. Although a large number of fiscal policy measures were launched in the current year to cushion the impact of high energy prices, the budget deficit will nevertheless narrow significantly as coronavirus-related measures expire and nominal GDP rises strongly. The discontinuation of crisis-related measures will further improve the situation of public budgets. However, they will continue to run deficits throughout the forecast period. The general government deficit is expected to be EUR 73 billion in 2022, EUR 51 billion in 2023, and EUR 42 billion in 2024.

Global Economy in Downturn

The global economy is in a downturn. The war against Ukraine that broke out in February of this year and Western sanctions against Russia have once again fueled inflation for energy commodities; Europe, where disappearing gas supplies from Russia can be replaced only to a small extent, is now struggling with an energy crisis. High inflation rates have prompted the US Federal Reserve and many other central banks to tighten monetary policy decisively. In China, the strict zero-covid strategy repeatedly prompts the government to prevent economic activity through lockdowns. In addition, a real estate crisis is simmering in China, weighing on the country’s construction sector and financial system. Weakening global demand should contribute to a softening of prices for industrial goods and a gradual easing of global supply chain problems. However, the processing of existing orders is still supporting the economy for the time being.

Against this backdrop, the institutes expect global production to grow by 2.5 percent this year and 1.8 percent next year. Only in 2024 is it likely to be stronger again, at 3.0 percent. Global trade in goods will expand at a rate of 1.6 percent in 2023, less than half the rate this year. Inflation will remain very high next year, particularly in European countries, and is not expected to ease appreciably until 2024. The institutes expect GDP in the United States to grow by 3.1 percent this year, by 0.6 percent in 2023, and by 2.5 percent in 2024. GDP growth in the EU is expected to be 3.1 percent in 2022, 0.1 percent in 2023, and 2.2 percent in 2024.

Risks

- Gas Availability

- Coronavirus Pandemic

Downloads and Links

-

Full-length version (in German)PDF / 2,61 MB / nicht barrierefrei

-

Key Forecast Figures for Germany

-

The Main National Accounts DataPDF / 236,27 KB / nicht barrierefrei

-

Sector Accounts for Institutional SectorsPDF / 194,04 KB / nicht barrierefrei

-

Press Release with Key Forecast Figures (PDF)PDF / 152,25 KB / nicht barrierefrei

-

Press Release

{kind=link}