Joint Economic Forecast Spring 2022: From Pandemic to Energy Crisis – Economy and Politics under Permanent Stress

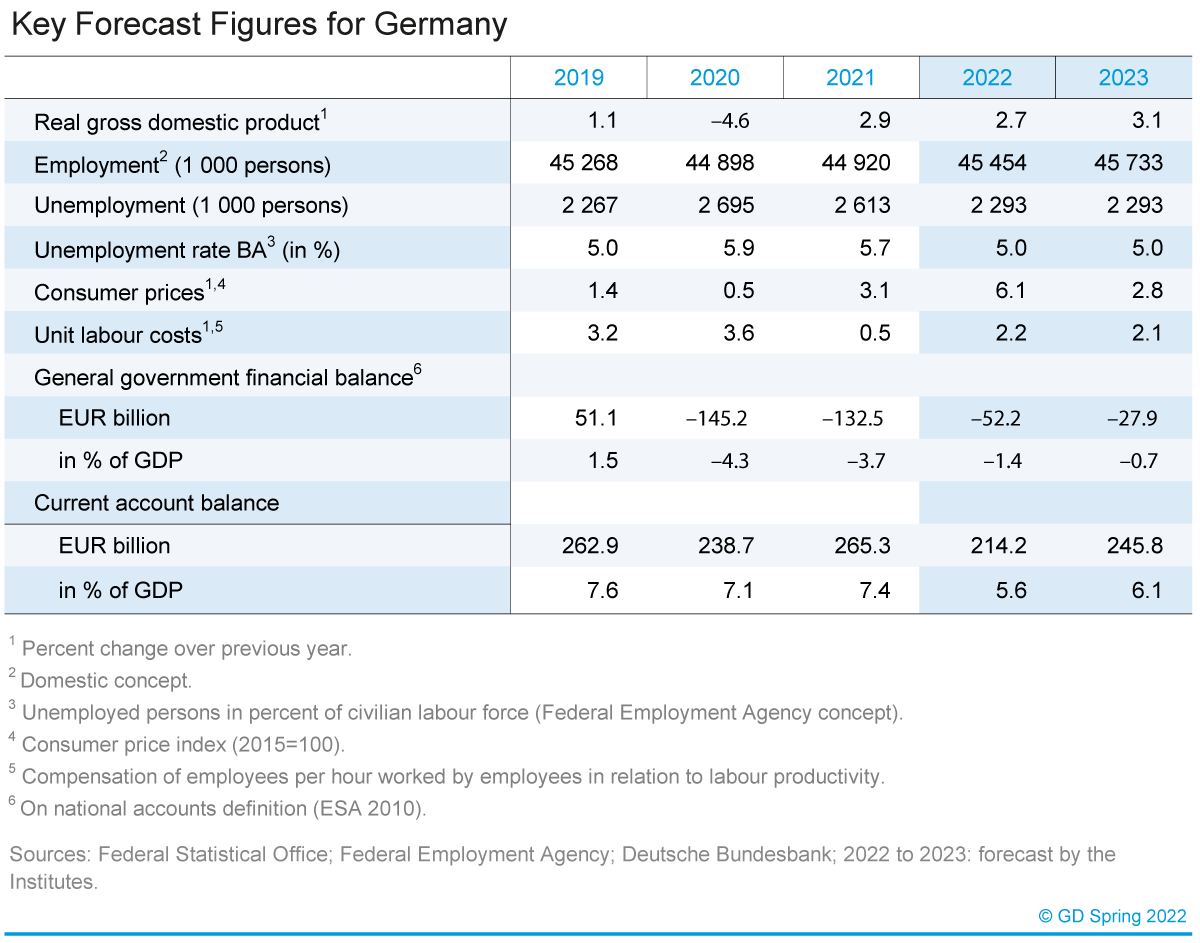

The German economy is steering through difficult waters. The upward forces resulting from the abolition of pandemic restrictions, the aftermath of the coronavirus crisis, and the shock waves caused by the war in Ukraine are creating opposing economic currents. Common to all influences is their price-driving effect. Accordingly, the pre-crisis level of economic output will not be reached until the third quarter of the current year. All in all, the institutes expect GDP to increase by 2.7 percent this year and 3.1 percent next year.

War in Ukraine Dampens Recovery

The now waning pandemic is accompanied by a strong recovery in its own right. This is being driven in particular by the contact-intensive service sectors. Industrial production has been on an upward trend again for five months now, although supply bottlenecks still hamper industrial activity. High demand coupled with inhibited supply is resulting in stronger price pressure. To the extent that supply bottlenecks are gradually overcome, the catch-up effects in manufacturing also give rise to expectations of a self-sustaining upswing.

The strong recovery that began in the spring, when the pandemic and its aftermath were overcome, was initially slowed by the outbreak of war in Ukraine. The war and the political responses are having a negative impact on economic activity through various channels on the supply and demand side. The loss of export markets, which is linked in particular to the Western sanctions regime against Russia, is noticeable but of secondary importance in macroeconomic terms. More significant is the massive increase in uncertainty about raw material supplies, especially – but not only – for key energy commodities, which has further fueled the upward price trend that was already underway before the Russian invasion of Ukraine. As a result, correspondingly more purchasing power is flowing abroad via the higher energy import bill, weakening demand in Germany. At the same time, the disruptions caused by the war are leading to new supply bottlenecks, which will affect not least the automotive industry in the short term.

At a rate of 6.1 percent, consumer prices are rising more strongly in the current year than at any time in the past 40 years. Next year’s rate of 2.8 percent will also remain well above the average since reunification. The process of accelerated inflation began a year ago already, and the war in Ukraine is exacerbating the upward pressure on prices. The sharp increases in commodity prices are only gradually reaching the consumer level. However, it is not only higher energy prices that are driving inflation. Domestic price pressure – measured by the GDP deflator – is increasing significantly in both forecast years at over 3 percent, and the core rate of inflation is also likely to remain at 3.1 percent in the coming year. Overall, broad-based price pressure has built up, which will continue to have an impact even if, as assumed, raw material prices ease again somewhat and supply bottlenecks in the second half of the year successively decrease.

The labor market is proving robust in the face of the strains on economic activity resulting from the war in Ukraine, as the delayed recovery of production is likely to be largely absorbed by working hours. The number of people in employment will continue to rise over the forecast period, albeit at a slower pace.

The jump in the minimum wage to EUR 12 this year will also contribute to this. Due to aging, a slowdown in employment growth is expected toward the end of the forecast period.

However, this will be countered by the assumed forced migration from Ukraine, which will increase the labor supply somewhat. The unemployment rate will fall from 5.7 percent in the previous year to 5.0 percent in both forecast years. Nominal wages are accelerating perceptibly, but will entirely prevent a loss of employees’ purchasing power in the forecast period.

In the current year, public budgets are expected to show a significantly smaller deficit of EUR 52 billion than in the previous year (EUR 132 billion). A major contribution to this will come from the fact that government spending will increase only a little in the wake of the expiry of pandemic-related corporate aid. At the same time, government revenue is rising as the economy recovers. In 2023, with strong wage growth and a robust labor market, revenue is expected to rise much faster than spending, reducing the deficit to just under EUR 28 billion or 0.7 percent as a share of GDP. This assumes that the funds from the credit-financed special funds, which are mainly earmarked for climate protection and defense, will flow out only to a small extent in the forecast period.

Economic Policy Still in Crisis Mode

Economic policy remains in crisis mode. Although the coronavirus measures are coming to an end, the war in Ukraine has added new challenges. The immediate consequences are seen in further increases in energy and other raw material prices, possible short-term supply bottlenecks, as well as increasing numbers of refugees.

Let Higher Energy Prices Take Effect

From an economic policy perspective, there is much to be said for letting the price signals work. Higher prices motivate companies and households to use scarcer resources more sparingly. Short-term consequences at affected companies should be cushioned and financial support for households should be limited to low-income households.

Global Economy: Recovery Slows

The war in Ukraine and the extensive sanctions against Russia have noticeably clouded the global economic outlook. While the purchasing power of consumers is reduced by high energy prices, geopolitical risks are weighing on companies’ willingness to invest. In addition, the problems in supply chains can repeatedly lead to faltering industrial production. The remaining restrictions in the fight against the pandemic may have only a minor impact on economic activity. China, on the other hand, will probably continue to adhere to its particularly strict containment policy, which repeatedly leads to the sealing off of entire cities and closures of factories or port facilities. This will help to ensure that problems with international supply chains remain in place for at least the first half of 2022.

Under these circumstances, the pandemic-related production constraints in China and, above all, the war in Ukraine will slow down the global economic recovery in 2022, but will not bring it to a halt. For the second half of the year, the institutes expect the coronavirus crisis to subside in China and energy and raw material prices to gradually decline. For this reason and also because of the weaker economy, inflationary pressure will then gradually ease. The institutes expect global output to grow by 3.5 percent this year and by 3.0 percent in 2023. Global trade in goods is expected to increase by around 3.3 percent this year despite only weak growth over the course of the year. For the coming year, the institutes expect an increase of 3.1 percent with slightly higher momentum over the course of the year. For the United States, a growth rate of 3.6 percent is expected for this year. Growth in the EU is expected to be 3.3 percent.

Gaslücke in Deutschland?

Sonderauswertung (Juni 2022)

Die Gaslücke, die sich bei einem sofortigen Stopp russischer Erdgaslieferungen noch im April ergeben hätte, besteht nicht mehr. Trotz mittlerweile deutlich besser gefüllter Gasspeicher sind damit aber noch nicht alle Risiken für die Gasversorgung der Industrie im Winterhalbjahr 2022/2023 gebannt. Es ist daher ratsam, zeitnah die Preissignale bei den Verbrauchern ankommen zu lassen. In der Sonderauswertung wurden Szenarien sowohl mit 0% als auch mit 40% Gaslieferungen aus Russland simuliert.

Sonderauswertung (Juli 2022)

Das zeitliche Profil der Gasverfügbarkeit und der Speicherfüllstände für eine Drosselung auf 20% zeigt, dass die Speicher im Median der Ergebnisse bis Ende 2023 positive Füllstände aufweisen und damit die industriellen Verbraucher nicht rationiert werden müssen.

Risks

- War in Ukraine

- Refugee movements

- Inflationary dynamics

- Pandemic waves impacting international supply chains

- Embargo of crude oil/natural gas

Downloads and Links

-

Full-length version (in German)PDF / 2,76 MB / nicht barrierefrei

-

Key Forecast Figures for Germany

-

The Main National Accounts DataPDF / 135,76 KB / nicht barrierefrei

-

Sector Accounts for Institutional SectorsPDF / 101,46 KB / nicht barrierefrei

-

Press Release with Key Forecast FiguresPDF / 218,78 KB / nicht barrierefrei

-

Sonderauswertung zur Gefahr einer Gaslücke in Deutschland (Juni 2022) (in Germa…PDF / 753,72 KB / nicht barrierefrei

-

Sonderauswertung zur Gefahr einer Gaslücke in Deutschland (Juli 2022) (in Germa…PDF / 343 KB / nicht barrierefrei

{kind=link}