Joint Economic Forecast Autumn 2021: Crisis Is Gradually Being Overcome – Align Action with Lower Growth

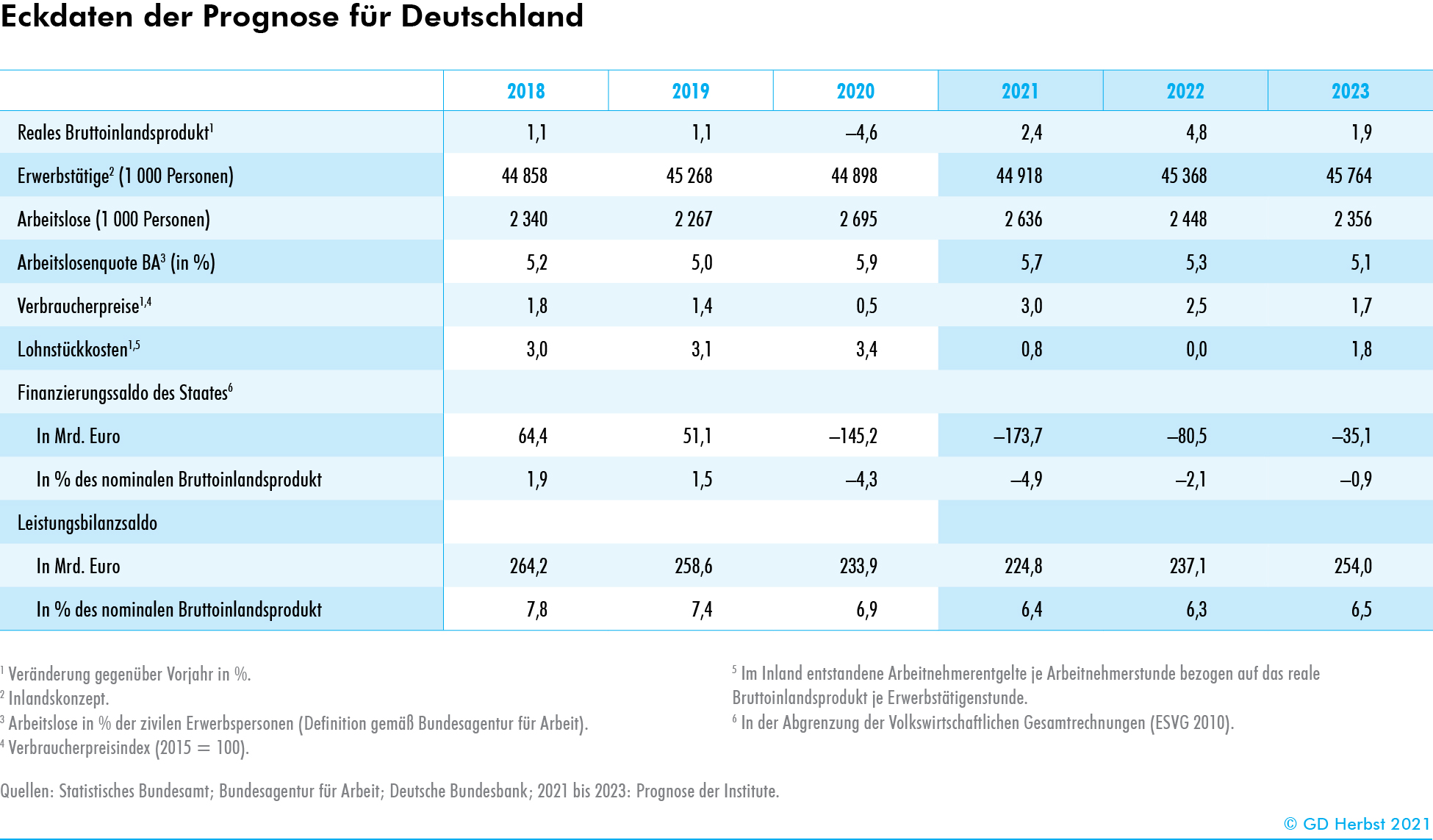

The economic situation in Germany continues to be marked by the coronavirus pandemic. A complete return to normal in contact-intensive activities is not expected in the short term. In addition, supply bottlenecks are hampering the manufacturing sector for the time being. In the course of 2022, the German economy should return to normal capacity utilization. According to the institutes’ forecast, gross domestic product will increase by 2.4 percent in 2021 and by 4.8 percent in 2022.

Private Consumption Marked by Catch-Up Effects

The coming quarters will be characterized by a further economic catch-up process. Private consumption is likely to return to normal over the course of the coming year as infection rates subside, even if the pace of growth is likely to slow down once again over the winter half-year. The institutes assume that once the pandemic-related impairments have ceased, some of the surplus savings that private households have accumulated due to a lack of opportunities for consumption will be spent, resulting in strong consumption momentum after the winter. With a growth contribution of 3.9 percentage points, private consumption will thus be the main driver of the strong expansion in output in 2022.

Production in the manufacturing sector will also increase again as supply bottlenecks ease. This allows for stronger corporate investment activity as well, especially as the economy’s capacity utilization rate is expected to pick up more strongly in the coming year. All in all, capacity is likely to be moderately overutilized in both 2022 and 2023; toward the end of the forecast period, the German economy is likely to gradually return to its potential path, with quarterly rates returning to normal.

The prospects for further economic recovery are supported by current developments on the labor market. Following the decline that accompanied the economic slump in 2020, employment is rising again; growth was particularly strong in the third quarter of 2021 at around 240,000 people. As the recovery continues, employment will continue to rise; the unemployment rate is expected to fall to 5.7 percent this year and 5.3 percent next year.

Consumer price inflation, currently well above the long-term average, is expected to remain elevated for the time being. The recent rise in energy prices, like inflation in many intermediate products, is likely to be reflected in consumer prices with a time lag. In addition, it is foreseeable that climate protection measures will cause prices to rise. The institutes expect consumer prices to rise by 2.5 percent in 2022 and by 1.7 percent in 2023, after 3 percent in the current year.

Fiscal policy is likely to shift to a significantly restrictive course as Covid-19 aid measures expire, even if the formation of a new government means there is increased uncertainty about fiscal policy measures in the forecast period. A return to a balanced budget, however, is not to be expected for the time being even with the achievement of normal capacity utilization – not primarily due to the consequences of the coronavirus pandemic, but rather because of the permanent increases in spending that were set in motion during the previous legislative period. The public budget deficit is likely to decline from 4.9 percent of GDP in the current year to 2.1 percent and 0.9 percent in the two following years. In view of the strong increase in nominal GDP, the public debt ratio is nevertheless likely to decline from just under 71 percent in 2021 to 67.3 percent in 2022 and 64.9 percent in 2023.

Economic Policy: Leaving Crisis Mode

With the recovery from the economic consequences of the coronavirus crisis, economic policy can leave crisis mode again. It is expected that normal capacity utilization will be reached again in the middle of next year. The focus must now be on the 2020s. These are characterized by a significant slowdown in potential growth as a result of demographic developments. At the same time, there are major challenges, such as reducing carbon emissions, stabilizing the pension system, and accelerating digitalization.

These macroeconomic challenges have been addressed too hesitantly so far. The current climate protection policy is inefficient and it is foreseeable that the emission targets the government set itself cannot be achieved with the measures now in place. In view of demographic change, the benefits promised in the statutory pension insurance system will soon be such a financial burden that they will crowd out other government spending and further increase the tax burden. Germany is lagging behind in digitalization and thus runs the risk of losing international competitiveness and failing to exploit opportunities to boost productivity. Germany’s next federal government has the opportunity to realign economic policy, shifting the focus from short-term consumerism to investment in human, environmental, physical, and social capital. In all of this, the sustainability of public budgets must be kept in mind.

Overcoming the coronavirus crisis also removes the basis for activating the exception clause in the debt brake. Admittedly, at its meeting in June this year the Stability Council took the view that an exceptional emergency situation within the meaning of Article 109 of Germany’s Basic Law could also be established for 2022, thus permitting an extension of the suspension of the debt brake. However, capacity utilization in itself no longer justifies this. Moreover, the German government has considerable reserves at its disposal.

Even if compliance with the debt brake imposes limits on public finances, there is currently scope to bring about a realignment of economic policy. For example, the tax ratio has risen in recent years, to 46.5 percent in pre-crisis 2019. This means that there are opportunities to reprioritize even within government budgets through reallocation. If the funds are used for productive investments, this can generate growth effects.

Global Economy: Pandemic Continues to Shape the Economy

The global economy is continuing to recover. However, expansion in 2021 was stagnant until into the autumn, and the overall pace is only moderate. Only in a few countries, such as the United States, has production returned to its 2019 level. The pandemic continues to weigh on economic activity in some places due to ever new waves of infection, most recently especially in places where vaccination progress is still insufficient. In addition, supply bottlenecks are putting the brakes on the upswing in global industrial production, which had been very strong until the beginning of this year but has now come to a standstill. Together with an increase in aggregate demand, the bottlenecks have contributed to a sharp rise in inflation in recent months. In the coming months, the pandemic will have a noticeable impact on the economy, especially in areas where vaccination rates are still low. As vaccination progresses, however, conditions should continue to improve. However, supply bottlenecks, which will probably be resolved only in the course of 2022, will act as a brake. For the US, a high growth rate of 5.6 percent is expected for this year, due not least to strong fiscal stimuli. Growth in the EU is only slightly behind at 4.9 percent in 2021. In China, where overall economic production is no longer significantly below the pre-crisis trend on the one hand and, on the other, the containment of stability risks requires a more restrictive economic policy course, the increase in output is likely to weaken over the forecast period. The institutes expect global production to grow by 5.7 percent this year and by 4.2 percent in 2022.

Risks

One of the (global economic) risks remains the possibility that new virus variants will again require more stringent infection control measures. The financial consequences of the pandemic are also uncertain. It remains to be seen how the solvency of companies will develop when government credit programs and debt moratoria expire. The consequences of the financial problems of individual large Chinese conglomerates are also unclear at present. Another factor of uncertainty for the economy is the savings accumulated by private households during the crisis. If these savings were to be used to a significant extent to catch up on consumer spending, it can be assumed that this would translate into further accelerated inflation. The current level of inflation is not just the result of temporary bottlenecks in supply chains and higher energy costs. Rather, bottlenecks in the labor market are already emerging, which could lead to stronger wage increases than assumed in this forecast

{kind=link}